Lihat juga

12.05.2026 11:05 AM

12.05.2026 11:05 AMYou get used to everything — the good and the bad. Markets have adapted to the Middle East conflict. Equity indices keep hitting new record highs, and the old slogan TACO ("Trump Always Chickens Out") has been replaced by a new quip: NACHO — "Not a Chance Hormuz Opens." Investors now assume that the world's main oil artery won't reopen until the economic damage from a blockade becomes catastrophic. So far, that outlook hasn't stopped the S&P 500.

Retail investors are confident that blockbuster corporate earnings provide a cushion against geopolitical shocks. According to JP Morgan, flows into chip-focused, equity-oriented funds hit a one-year high in the week to May 8. As a result, the Philadelphia Semiconductor Index climbed to a record high.

Philadelphia Semiconductor Index Performance

The higher the S&P 500 climbs, the more bulls enter the market. HSBC raised its year-end 2026 target for the broad index from 7,500 to 7,650, while CFRA lifted its target from 7,400 to 7,575. The most aggressive call comes from Yardeni Research, which sees the index at 8,250 versus its prior 7,700. The drivers cited are improving sentiment around AI technologies, ongoing AI adoption across the economy, and an easing of risks related to geopolitics, trade, and interest rates.

Citi argues that big-tech corporate earnings are the main engine behind the S&P 500's strength. The broad index is up 8.4% year-to-date, while the Nasdaq 100 has gained 16%, driven in large part by heavy semiconductor purchases.

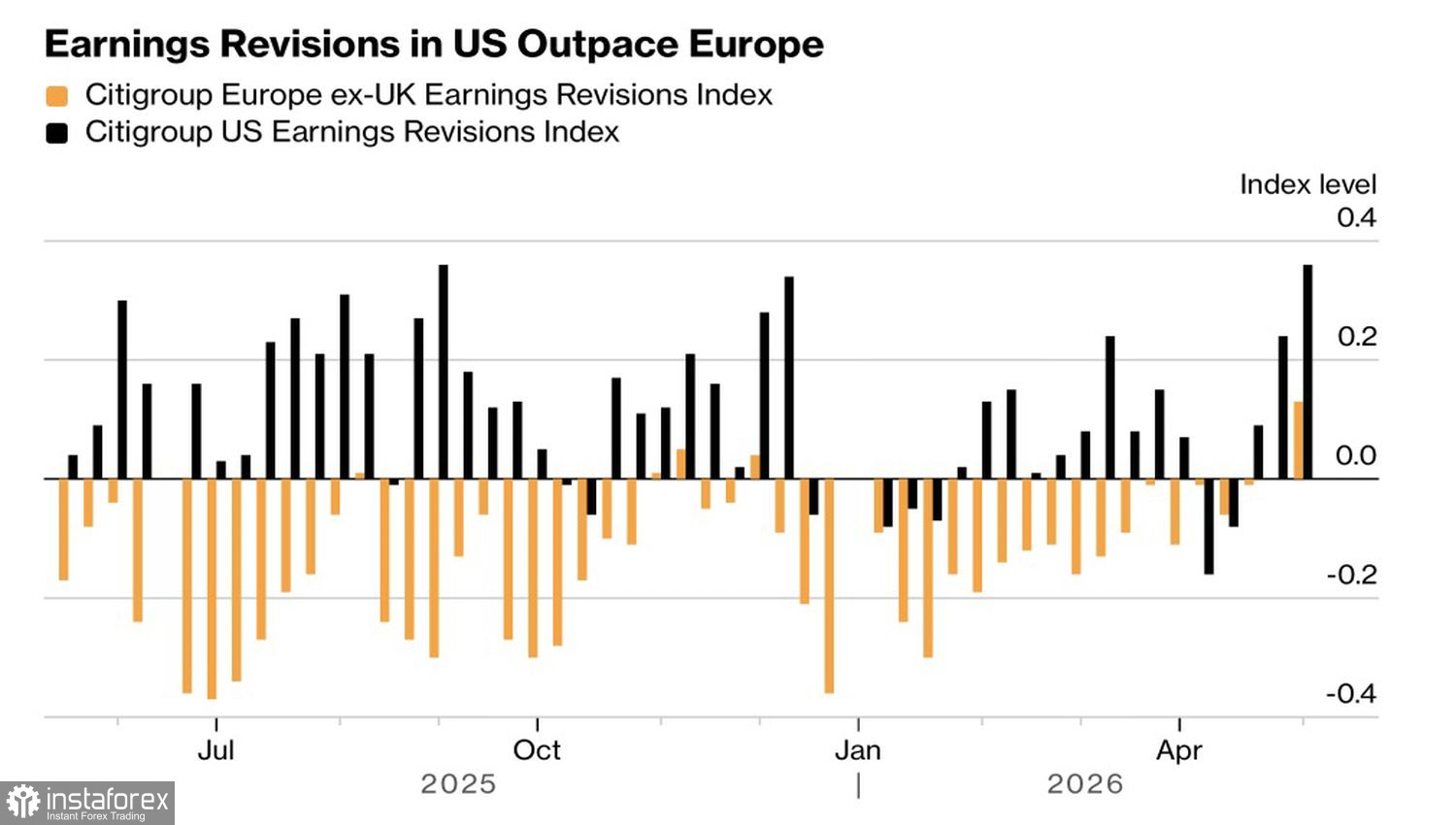

US vs Europe Earnings Revisions Dynamics

The technology sector accounts for 37% of the S&P 500 versus just 6.3% of the EuroStoxx 600. It is therefore unsurprising that US companies are beating profit forecasts by a wider margin than European issuers. As a result, capital is flowing from the Old World to the New, which is a key driver of the broad-market rally.

The market now faces a test from US inflation data for April. CPI is expected to quicken to 3.6%, which would raise the odds of higher Fed funds rates. The market currently prices in roughly a 30% chance of a rate increase by end-2026 and about 50% by April 2027. Tighter monetary policy would likely push Treasury yields higher and raise borrowing costs for US corporates. The question is whether the equity market can absorb that burden.

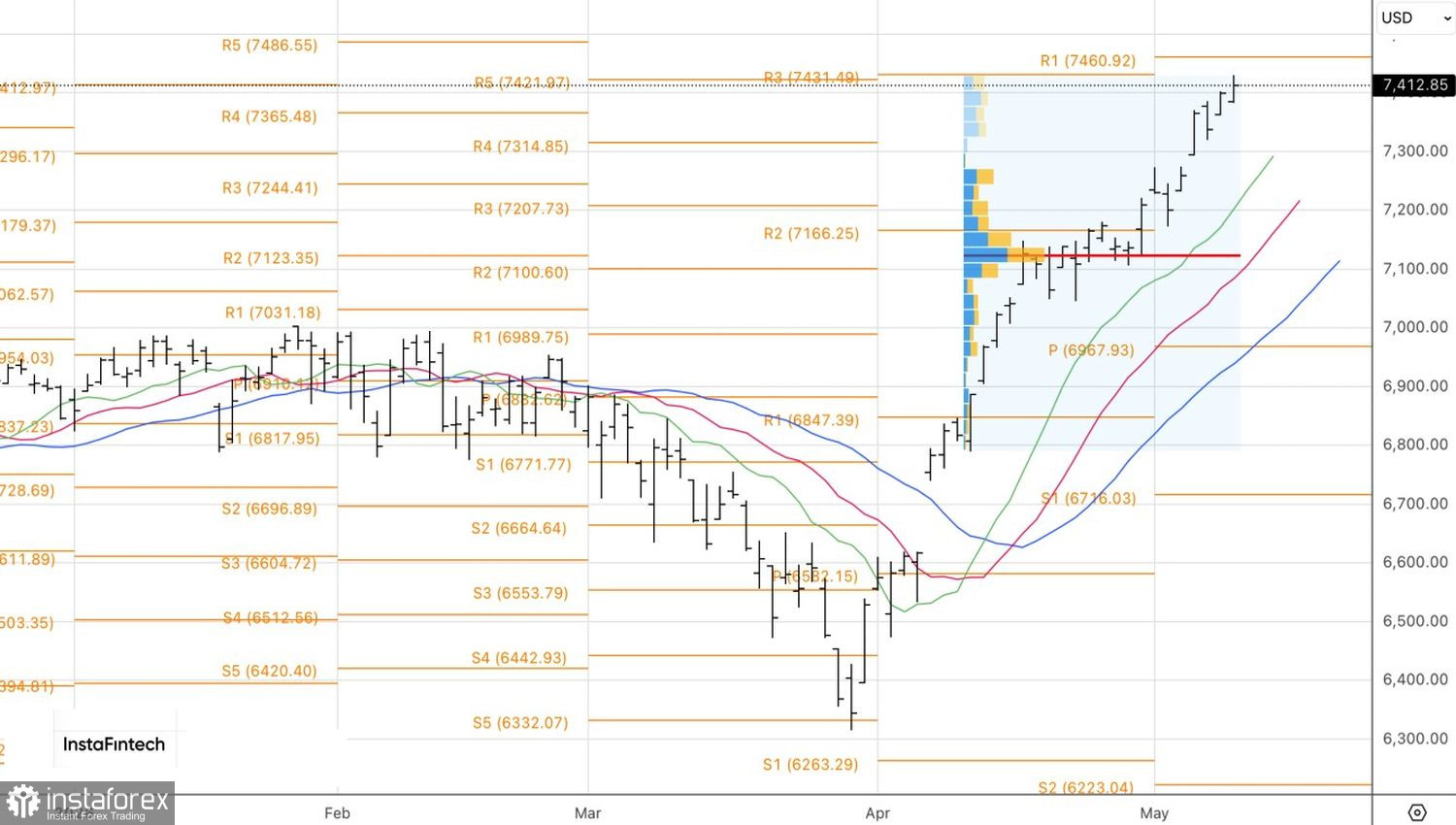

Technically, the daily S&P 500 chart shows the uptrend continuing toward a convergence zone limited by the levels of 7,435 and 7,460. Failure to overcome that zone would likely trigger a pullback, thus creating the usual buying-the-dip opportunity for traders.