यह भी देखें

28.04.2026 12:48 AM

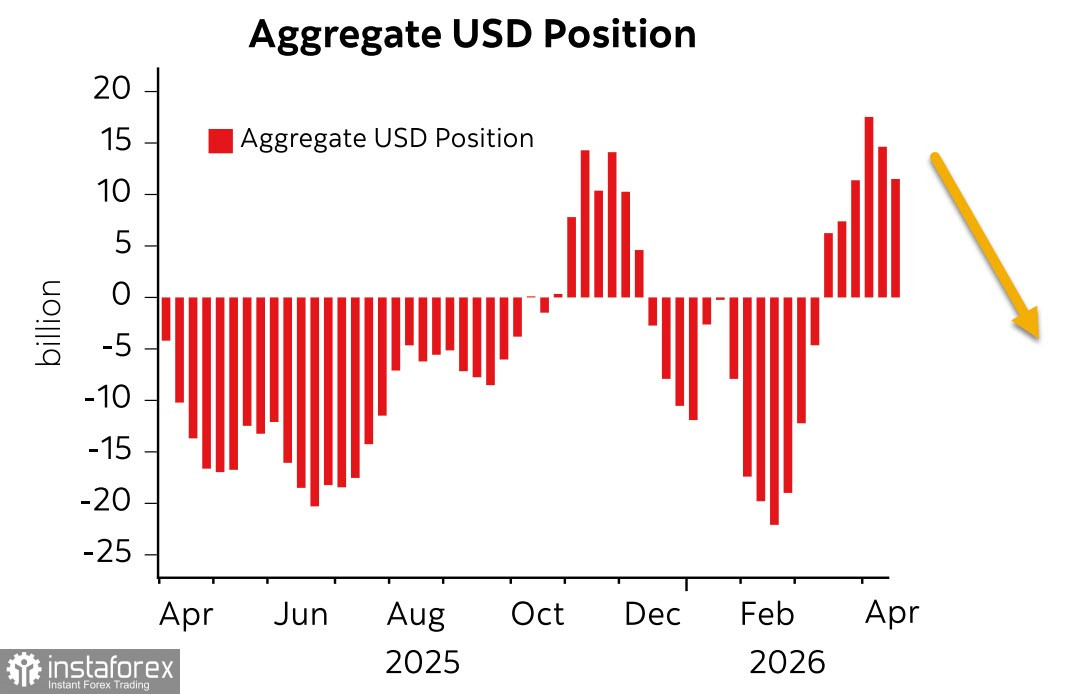

28.04.2026 12:48 AMThe cumulative long position in the U.S. dollar against major global currencies decreased by $3.1 billion over the reporting week, down to $11.6 billion, marking a decline for the second consecutive week. It is evident that this shift in positioning is driven by hopes for an end to the war in the Middle East.

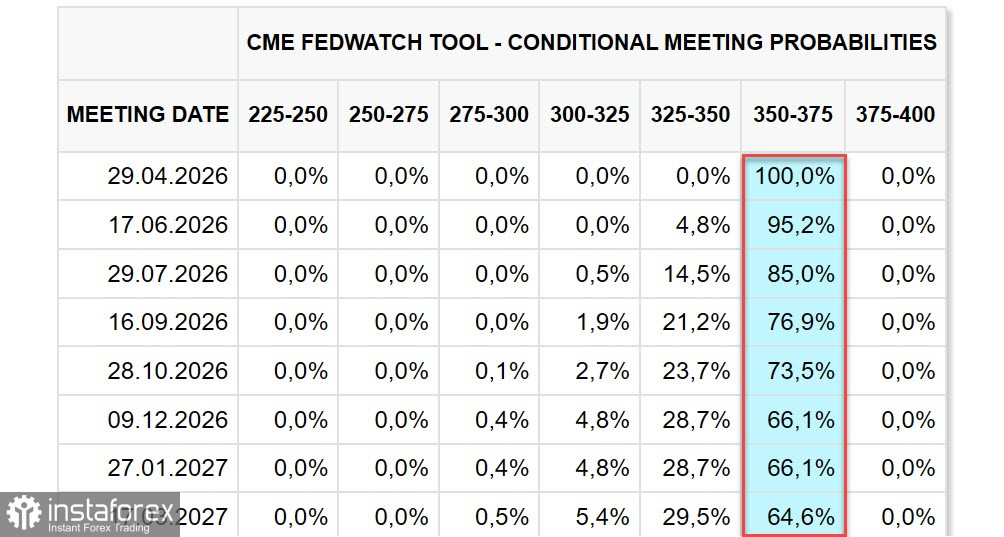

On Wednesday, the Federal Reserve will hold its next monetary policy meeting, and it is expected to keep interest rates unchanged. The risks that the Fed has to consider in making its decision appear balanced. On the one hand, inflation remains above target, and the energy crisis stemming from the war in the Middle East could push it even higher. On the other hand, job growth in the US has certainly slowed in recent years, and the unemployment rate is relatively stable, which practically means that the monthly job increase could be close to zero without an increase in unemployment. If this dynamic changes, then it might suggest the need for rate cuts, but not now; futures do not anticipate any changes for at least the next year.

For the dollar, the situation looks increasingly clear. When positive news arises from the Middle East, the dollar weakens, and risk appetite increases. Conversely, when it becomes apparent that negotiations have hit a deadlock again, both the dollar and oil prices rise while demand for risk decreases. The market has clearly demonstrated this mechanism.

We must proceed from the premise that hopes for a successful resolution of the war are becoming increasingly elusive. Washington has not achieved the desired outcome on the battlefield and is pursuing its goals through negotiations. Iran has not lost this war and is not acting from a position of weakness. This situation could last for a long time, and the longer the uncertainty persists, the more pronounced the consequences will be. The energy crisis could simultaneously trigger two effects: rising inflation and, shortly thereafter, a global food crisis, as fertilizer production has sharply slowed due to a lack of natural gas. In the long run, these factors favor the dollar, but in the short term, they do not.

We assume that the resumption of active hostilities under current conditions is unlikely, meaning the dollar cannot rely on this factor. Ongoing tension will prevent the dollar from falling, so it will trade within a narrow range with a tendency to weaken against major currencies. If tensions decrease, the process of dollar weakening will accelerate.